The Heist℠ Sweepstakes — Countdown to End

Up to $146,000 in Prizes!

High-interest debt isn’t just a financial problem; it’s a weight that presses down on every aspect of your life. It’s the knot in your stomach when you check your mail, the sleepless nights spent staring at the ceiling, and the quiet dread that you’ll never get ahead. You make payments, but the balance barely moves, swallowed by relentless interest charges. It can feel like drowning in slow motion.

But what if you were thrown a lifeline? A sudden $10,000 cash injection isn’t just money; it's an opportunity to break free. It’s a powerful tool that, if used strategically, can do more than just pay a few bills—it can dismantle the debt machine that has been working against you for years.

This isn't a guide for spending a windfall. This is a battle plan for using a $10,000 lifeline to achieve financial freedom.

Step 1: The Debt Inventory - Know Your Enemy

Before you can attack your debt, you must understand it completely. You cannot fight an enemy you cannot see. For the next 48 hours, your only job is to gather intelligence.

- List Every Debt: Create a spreadsheet or use a notepad. List every single creditor, the total amount owed, the minimum monthly payment, and—most importantly—the exact interest rate (APR). This includes credit cards, personal loans, medical bills, payday loans, and anything in collections.

- Calculate Your Debt-to-Income Ratio (DTI): Add up all your minimum monthly debt payments and divide that number by your gross monthly income (your income before taxes). Lenders use this number to gauge financial health. A high DTI (over 40%) is a major red flag.

- Pull Your Credit Reports: You are entitled to a free report from all three major bureaus (Equifax, Experian, and TransUnion) annually. Scrutinize them for errors and get a clear picture of how lenders see you.

This process can be stressful, but it’s non-negotiable. It replaces vague anxiety with cold, hard facts—and facts are the foundation of a winning strategy.

Step 2: The Strategic Choice - Consolidation, Settlement, or Direct Assault?

With $10,000 in hand, you have options that were previously unavailable. The three primary paths are debt consolidation, debt settlement, or a direct-payoff assault.

- Debt Consolidation: You take out a new, single personal loan to pay off multiple high-interest debts.

- Pros: One manageable monthly payment, and hopefully a much lower interest rate than your credit cards.

- Cons: You're not out of debt; you've just moved it. It requires a good enough credit score to qualify for a low rate.

- The $10,000 Role: The cash can serve as a massive down payment on the loan, reducing the monthly payment and making you a more attractive borrower.

- Debt Settlement: For accounts in collections, you can offer a lump-sum payment to "settle" the debt for less than the full amount owed. Collection agencies often buy debt for pennies on the dollar and may be willing to accept 40-60% of the balance in a single payment.

- Pros: Can make a large debt disappear for a fraction of the cost.

- Cons: It can negatively impact your credit score, and any forgiven debt may be considered taxable income.

- The $10,000 Role: Cash is king in negotiations. A $10,000 cash offer to settle a $20,000 collection account is a powerful bargaining chip.

- Direct Assault (The Debt Avalanche): This involves making a massive, targeted payment directly to your highest-interest debt.

- Pros: Guarantees you save the most money on interest. The debt is completely eliminated, not just moved.

- Cons: Requires discipline to continue attacking the remaining debts afterward.

- The $10,000 Role: This is the full force of your lifeline. A $10,000 payment on a credit card with a 25% APR will instantly save you $2,500 in interest payments over the next year alone.

Step 3: The Nuclear Option - Considering Bankruptcy

For some, the debt tsunami is too large for even $10,000 to solve completely. In these situations, the money can be used for the ultimate fresh start: bankruptcy. While it has serious consequences for your credit, it is a legal tool designed to help people who are truly overwhelmed.

- Chapter 7: Aims to liquidate assets to pay creditors, discharging most unsecured debts (like credit cards and personal loans).

- Chapter 13: A court-supervised repayment plan over 3-5 years.

The $10,000 Role: Filing for bankruptcy isn't free. You need to hire a qualified bankruptcy attorney. Legal fees can range from $1,500 to $4,000 or more. Your $10,000 lifeline could cover these legal costs entirely, giving you access to a legal process that could wipe out tens of thousands of dollars in debt and give you a true second chance.

Final Step: Rebuilding the Seawall

Once the immediate threat is neutralized, you must ensure the tsunami never returns. Use any remaining funds (or the newly freed-up cash flow from eliminated payments) to:

- Establish a $1,000 Starter Emergency Fund: This is your first line of defense against future debt.

- Create a Strict Zero-Based Budget: Every dollar of income is assigned a job, so you never overspend.

- Address the Root Cause: Seek financial counseling if necessary to address the habits that led to the debt in the first place.

Securing a $10,000 lifeline to execute a plan like this can feel like the hardest part. However, opportunities to gain that financial leverage do exist, sometimes when you least expect them.

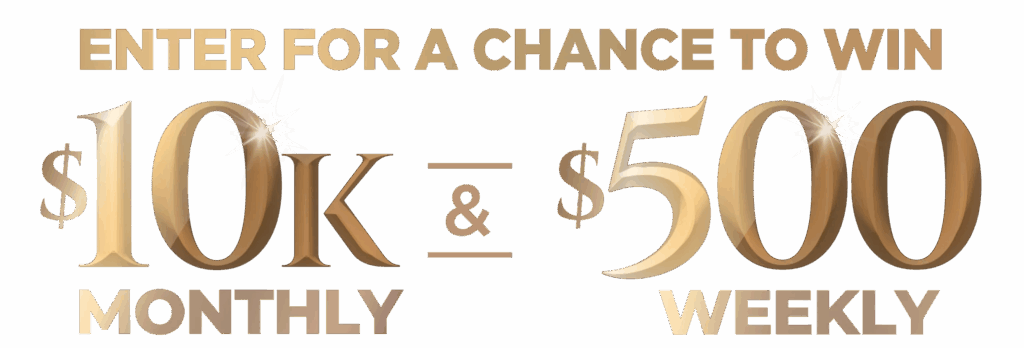

For those ready to launch their own attack on debt, "The Heist" sweepstakes presents a chance to acquire the capital needed to start fresh, offering substantial monthly cash prizes to winners.

Official Entry

ENTER HEREPrize Breakdown

- 12 Monthly Prizes: $10,000 Cash each

- 52 Weekly Prizes: $500 Virtual Prepaid Cards

- Total Prize Pool: $146,000

Giveaway Recap

- Sponsor

- ITG Brands, LLC

- Eligibility

- 21+ U.S. smokers (void MA & MI)

- Entry Methods

- Pack Codes or Mail-in Entry

- Promotion Period

- Oct 1, 2025 – Sept 30, 2026

- Drawings

- Weekly & Monthly through Sept 2026